Summary

- Earnings this year could still eclipse earnings of 2019.

- New business continues to be generated in all segments of the business.

- The present price of the firm's assets points to strong gains ahead.

- Looking for more stock ideas like this one? Get them exclusively at Elevation Code. Get started today »

Global Payments (NYSE:GPN) announced its first quarter numbers on the 6th of May last where the consensus number of $1.53 per share was beaten by $0.05. With second quarter numbers expected to be announced on the 3rd of August next, consensus is expecting $1.20 in earnings per share. The second quarter is expected to be the lowest of this fiscal year with $1.59 and $1.82 the expected bottom-line numbers, respectively, for Q3 and Q4, respectively.

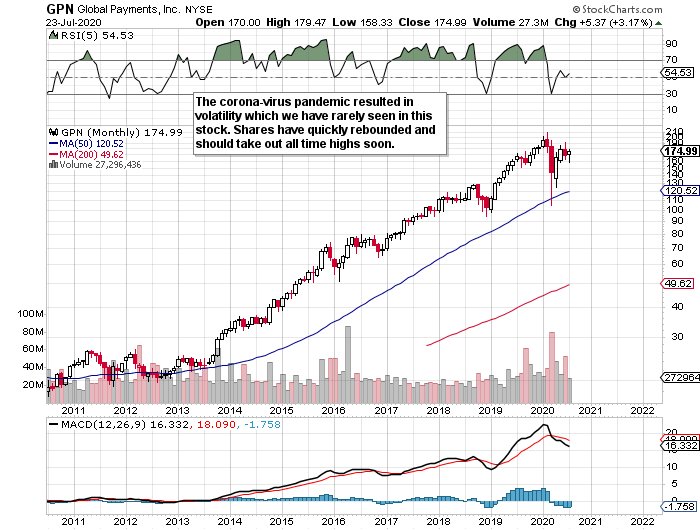

If indeed the firm can meet these expectations or even announce some earnings beats (as it has consistently been doing), then GPN could actually increase its annual earnings over 2019. Considering the environment many firms have had to deal with this year, this would be quite a feat for the payment and software firm. In fact, when we look at the long-term chart, we can see how sustained earnings growth has led to minimal volatility in shares in recent years. As we have discussed many times before, minimal volatility in long positions is the holy grail of long-term investing. Why? Because it is far easier to hold long positions for a sustained amount of time if drawdowns remain at a minimum.

Despite recent lockdowns and social distancing measures, for example, GPN still managed to close a sweet deal with Truist Financial Corporation (NYSE:TFC), which again demonstrated the growth markets GPN is at the cutting edge of. In fact, since the fundamentals of the firm are most definitely making themselves known on the technical chart, we would be very surprised if the all-time highs are not taken out here in the near term.

For example, Jeff Sloan on the first quarter earnings call pointed to the Synovus (NYSE:SNV) partnership, how software partners have been increasing, and how the firm's e-commerce and omni-channel businesses continues to go from strength to strength. Suffice it to say, GPN has the luxury of operating in multiple growth markets across a spectrum of different jurisdictions at present.

To get more insights on how we would view GPN as an investment at present, we look to the firm's profitability, valuation and how it has been rewarding shareholders in recent times. On the profitability side, GPN is well ahead of the sector when it comes to its operating margin of 19.5% and its gross profit margin of 55.4%. The latter profitability metric has slipped somewhat over the past five years (5-year average of 58.75%) but remains well ahead of the average (47.78%) in this industry. Management though is confident that ongoing synergies as well as cost initiatives will end up being a further tailwind for margins going forward.

Followers of our work will know that we do not give margins the precedence as many analysts on Wall Street, for example. Yes, we demand that any company we invest in is profitable, but margins usually take care of themselves when the valuation is right. As long as we believe that we are getting good value for the company's earnings, sales, assets, and cash flow, then the profit margins over time should have a bullish undertone.