Summary

- You might be interested in one of these two investment plays in the cable and broadcast industry.

- One is better for a buy and hold fundamental strategy.

- The other is a merger speculation stock that still has a chance at 80-100% gains if acquisition interest returns after the coronavirus pandemic ends.

In this article, I hope to give you a bird's-eye comparison of the relatively few publicly traded regional broadcasters remaining after a wave of industry consolidation and mergers and point out a couple of opportunities. If you are more interested in large, nationally reaching cable/media companies, you might be interested in my recent article on Fox (NASDAQ:FOX) (Owner of Fox News, Fox Sports, and as of recently Tubi) here.

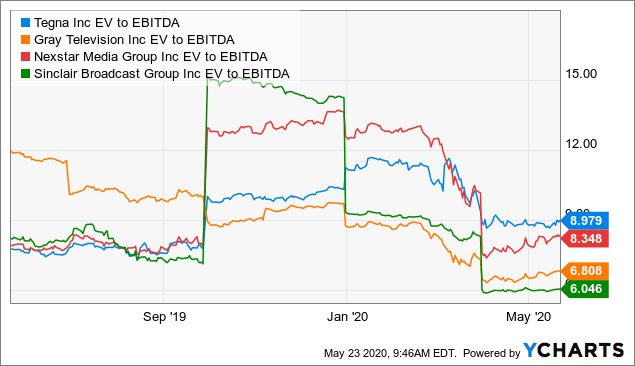

As we look at the valuation levels of the regional broadcasters, TEGNA (NYSE:TGNA) trades at the higher end of the industry while Gray Television (NYSE:GTN) and Sinclair (NASDAQ:SBGI) are both trading moderately below them in valuation. All valuations are using trailing EBITDA, assuming that their shared industry makes them similar enough to all be affected to a similar extent by the coronavirus pandemic.

Data by YCharts

Data by YChartsWe can put the valuations in context by looking at the debt level and profit growth of each company.

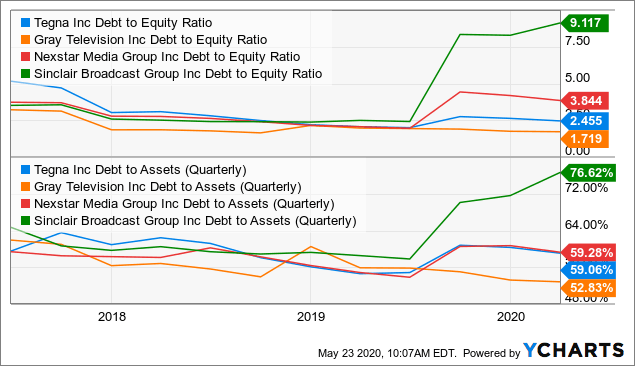

Data by YCharts

Data by YChartsWe can see that Sinclair is more leveraged than the others, which is likely why it trades the cheapest on an EV/EBITDA basis. Of the others, Gray is the least leveraged based on the debt to equity, debt to assets, and Debt/EBITDA ratios.

As far as judging growth, I believe EBITDA per share is the best metric to use. Revenue growth can get distorted because frequent M&A transactions complicate determining what growth is recurring organic growth or what is from an acquisition. Using a per-share metric to compare earnings growth is also important because it doesn't altogether exclude M&A transactions. The metric can account for shareholder accretive acquisitions that fuel per-share growth and penalize companies that have destroyed shareholder capital through dilutive M&As. Free cash flow is the metric that ultimately matters, but capital expenditure cycle differences create short-term distortions in the number. So, to measure medium-term growth in profit, we can measure it on an EBITDA per share basis.