Summary

- Today we revisit Stemline Therapeutics, whose stock has fallen some 35% this month on disappointing preliminary Q4 revenue guidance.

- However, the company's ELZONRIS franchise and the stock still have a bright long-term future.

- We update the investment thesis on this small oncology concern in the paragraphs below.

- I do much more than just articles at The Busted IPO Forum: Members get access to model portfolios, regular updates, a chat room, and more. Get started today »

Nearly all men can stand adversity, but if you want to test a man's character, give him power." - Abraham Lincoln

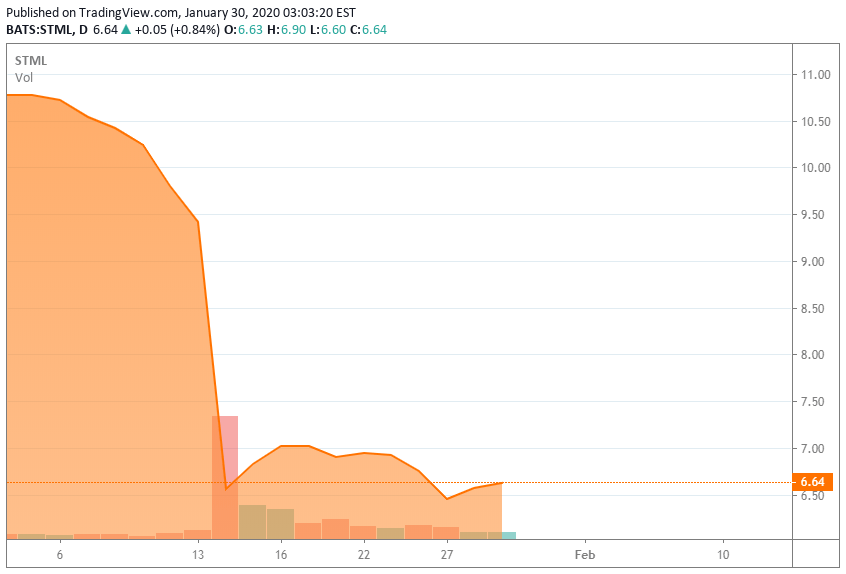

It has been a tough start to 2020 for Stemline Therapeutics (STML), or at least its stock. The shares dropped some 35% on January 13th when the company provided preliminary fourth quarter revenue guidance for recently approved ELZONRIS that did not live up to expectations. In this article, we take a look at recent events and update the investment case on Stemline in the paragraphs below.

Company Overview

Stemline Therapeutics is a small biotech concern based out of New York. The company has one approved product called ELZONRIS and its other clinical candidates include: SL-701, SL-801, SL-901, and SL-1001. Stemline Therapeutics currently has a market capitalization of roughly $310 million and trades for just over $6.50 a share.

Preliminary Fourth Quarter Guidance

Stemline provided preliminary Q4 ELZONRIS sales of just $11.8 million this Monday. Investors were obviously disappointed given Q3 sales of ELZONRIS came in at $13.3 million. This is more so given ELZONRIS' J-code designation came into effect on October 1st and should have boosted sales.

Management had this to say about the shortfall 'Given the orphan nature and unique features of this disease, we believe patient starts were subject to significant quarterly variance - a phenomena that will likely continue throughout 2020'. The market will be looking for further clarity on this during upcoming fourth quarter conference call which will be in early February. In its first full year on the market, ELZONRIS should do just over $43 million in total revenue.

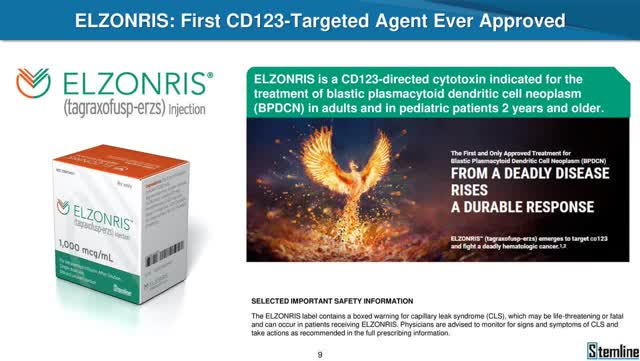

ELZONRIS is a novel targeted therapy directed to the interleukin-3 (IL-3) receptor-? (CD123), a target present on a wide range of malignancies including BPDCN, AML, certain myeloproliferative neoplasms (MPNs), myelodysplastic syndrome {MDS}, chronic myeloid leukemia {CML}, B-cell acute lymphoid leukemia (B-ALL), hairy cell leukemia, and Hod