Summary

- Akamai is a software company with a solid record of growth and high profitability.

- However, it is divided into two main lines of business, one which is poised to grow and one which will stagnate.

- Management is trying to tackle this problem through M&A.

- At the current price, we think the company is fairly valued and would consider adding a position for the long term.

Thesis Summary

Akamai (AKAM) is a software company providing cybersecurity and CDN to clients all over the world. The company has shown good and stable growth, has a strong financial position and is investor-friendly. However, its main source of revenue is under threat and it is likely that growth will slow-down.

Given the projected growth rates for the CDN and Cybersecurity segments of the business, we have projected revenues fro 2020 and 2021 and found the company to be fairly valued. While the company doesn’t represent an immediate value opportunity, we like the core business and would consider adding a position for the long-term.

Company Overview and Industry

Akamai is a software development technology company that recently celebrated the 20th anniversary of its IPO. The company is most well known for developing and implementing cloud security services and applications, as well as providing CDN. (Content Delivery Network). CDN’s are used by sites and organizations with large international traffic. When you enter a site, the CDN will recognize the user’s geographical area and will use the servers closest to the user to give access to the site. (To optimize speed and efficiency) In lamens terms, the company provides the infrastructure and software to deliver content quickly and also offers online security systems.

At first glance, I thought Akamai looked like a great investment. The best of both worlds, growth, and value. The company is in a growing and innovative space, both in terms of cloud computing and cybersecurity. Akamai achieved YoY growth in 2018 of 6.5% and has a CAGR of ~10%. Furthermore, the company is very profitable, boasting an EBITDA margin of 28.4%.

The company is run, in a very investor-friendly way, and indeed has active investors such as Elliot Management Corp. The company holds a strong balance sheet, is responsible for costs and returned value to investors through buybacks in 2018.

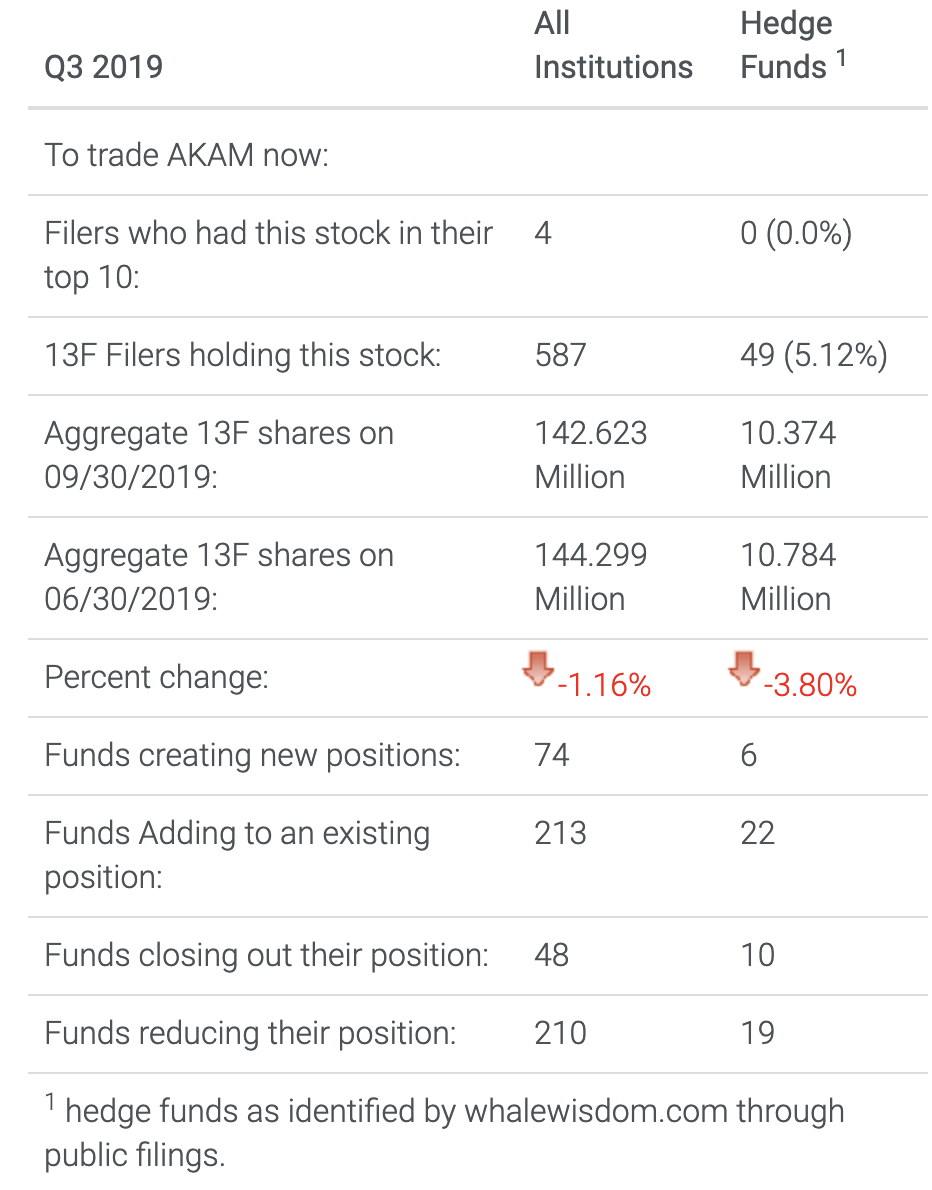

Indeed, we can see institutional support was strong for Akamai., but this seems to have changed.

Source: Whalewisdom

The above screenshot from Whalewisdom shows that, on the whole, financial institutions have reduced their position in Akamai. So what could be behind this change in sentiment?