- COKE looks like a classic example of an overvalued company with a high P/B and low ROE.

- The company is indebted and has no immediate plans to increase growth, while profitability is decreasing.

- I believe COKE still has a long way to drop and we could see the stock fall by another 50% in 2020.

Thesis Summary

Coca-Cola Consolidated, Inc. (COKE), is currently trading at incredibly high valuation ratios despite showing slowing growth and lower profitability. There are a few reasons for this and in this article, I will try and explain this overvaluation and reach a target price more in line with the intrinsic value of the company.

Company Overview

COKE, while being an independent entity, can be seen as a subsidiary of The Coca-Cola Company (KO), which owns a substantial majority of the firm. However, COKE is not involved in the production of Coke, it is only involved in the bottling and distribution of non-alcoholic beverages, but mostly Coke. COKE is the largest one of many distribution partners that work with The Coca-cola company.

The company was formerly known as Coca-Cola Bottling Co, changing its name in January 2019 and leading many investors to confuse COKE with KO. This confusion can be seen as one of the contributing factors to COKE’s lofty valuation.

Since its “rebranding” in January Coca-cola Consolidated enjoyed a massive price rally which took the stock from ~$170 to nearly $400 in May. Since then the stock has steadily fallen to a price today of $272.

Why I think COKE is overvalued

While it is very plausible that, indeed, as pointed out by fellow SA author Pedro de Noronha, some (amateur) investors have confused COKE with KO, leading to the price appreciation, we can also build a much more solid argument as to why COKE is not worth $400 or even $272.

Lower profitability:

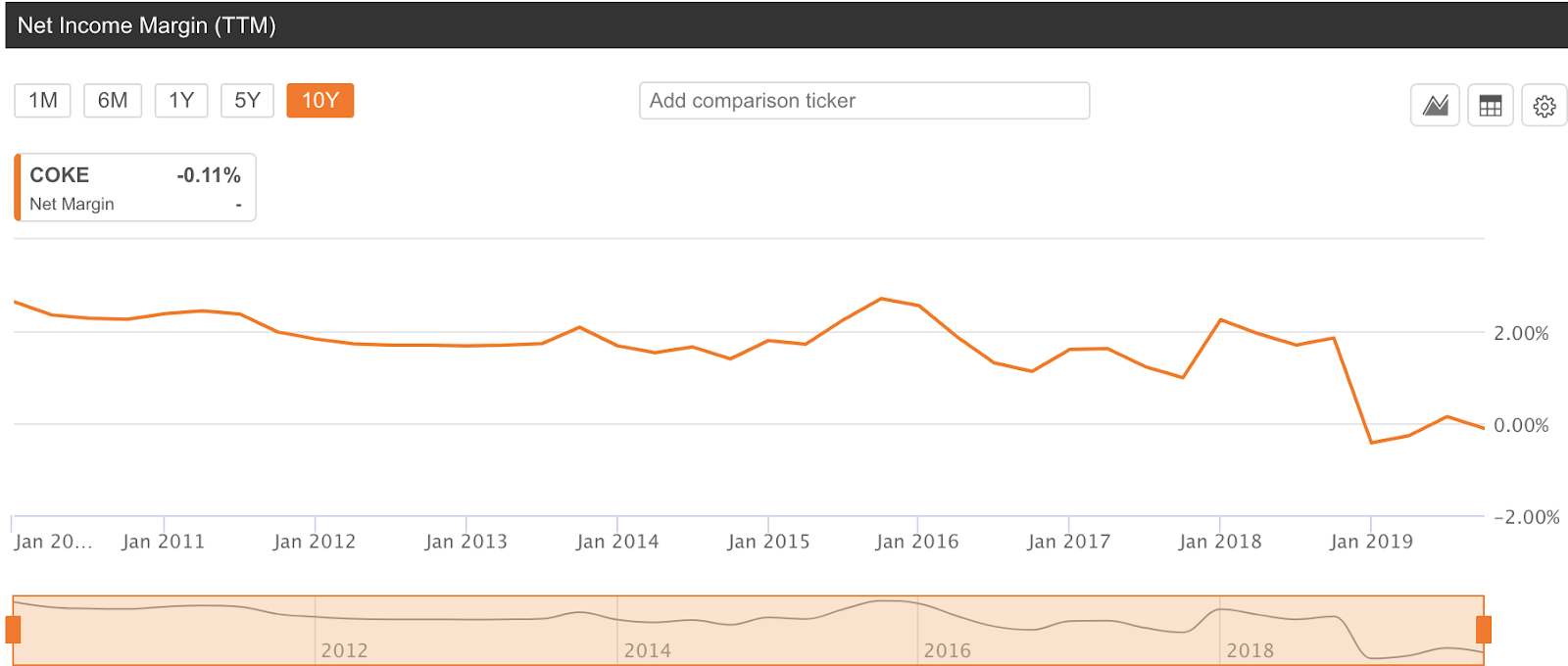

Unlike the actual CocaCola Company, CocaCola Consolidated is not a name that can command high margins. While some analysts have pointed to what looks like a reasonable 34% gross profit margin, COKE has consistently turned negative profits. In terms of Net Income margins, we can see how the company doesn’t look quite as attractive.

Source: SA

Not only is the current profit margin essentially 0%, but we can see a downward trend over the last 10 years. This can be attributed largely to the increasing cost of sales, which grew at about 10% in 2017-18 and increasing downward price pressure. Keep in mind, most of COKE’s sales can be attributed to a few large retailers such as Walmart, which hold a lot of bargaining power.