Summary

- Coca-Cola shares continue to trend upward and appear expensive trading near 52-week highs.

- The company is counted upon by many income investors for consistent performance.

- Shares at this time are expensive compared to peers and should not be bought.

Coca-Cola (KO) stock has long been looked upon by investors as a steady reliable investment. Each year the company would produce higher revenue and profits and share that by returning capital to stakeholders. However, Coca-Cola has been seeing declining revenue trends that are concerning. Investors looking for that reliable performance can probably still count on Coca-Cola, but at this time shares are quite expensive. For investors who would love to own a stake in the company, waiting for a pullback will be fundamental in driving returns.

Performance

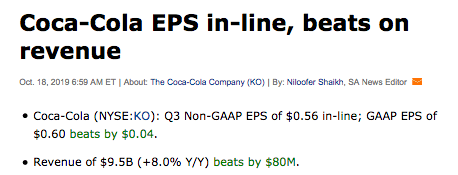

Coca-Cola just reported a rather nice quarter of results.

Source: Seeking Alpha

Source: Seeking Alpha

A beat on both the top and bottom lines was driven by strong organic growth. While most of this growth was attributed to new products in lines such as Smartwater and Fuze. Net revenues grew 8.% to $9.5 billion. However, organic growth was up about 5% which is still impressive given Coca-Cola's size. The company continues to see unit/case volume growth in all regions which is helpful to the overall picture. The company did see some margin pressure this quarter which was attributed to acquisitions and currency effects. I would expect continued margin pressure for the company in the future as well. Headwinds from increased commodity, labor, and freight costs have become frequent for many consumer packaged goods companies. The only way to expand margin is through cost cuts, higher selling prices, or acquisitions of companies with higher margins. The impact of an acquisition on Coca-Cola is usually small though.

So far cash from operations for the year has generated $7.8 billion, which is up a huge 37%. This increase was due to iniatives the company has taken as well as the timing of taxes. This led to cash flow thus far of $6.6 billion, up 41%. This is nice to see as the last time we reviewed the company cash flow was down. Increased cash flows mean better coverage ratios for debt and dividends. It also allows for more share repurchases.