Summary

- SunTrust's dividend growth over the last five years has been outstanding.

- The upcoming merger with BB&T is going to bring significant cost savings and potential synergies for capital appreciation.

- Despite net income compression in the short-term, there is great potential with the new bank, Truist.

SunTrust (NYSE:STI) had an ok Q2 2019, but the big news is the ongoing merger with BB&T (NYSE:BBT), which will bring significant cost savings and potential synergies to new the bank, Truist. Along with the merger, SunTrust has continued its ongoing trend of tremendous dividend growth over the last nine years.

Despite the current rate environment, which has seen the Fed lower rates and promising more in the future, SunTrust has been able to withstand the compression to net interest margin and show growth in its loan portfolio as well as investment income.

I think the new bank, Truist, has the potential to be a great, long-term holding for investors looking for capital appreciation and dividend growth.

Overview

SunTrust had a decent second quarter with earnings per share this quarter of $1.48, which was a 14% improvement from the previous quarter and up 1.3% YoY. Earnings were higher as a result of higher non-interest income and lower provision expenses.

Source: Q2 2019 Investor Presentation

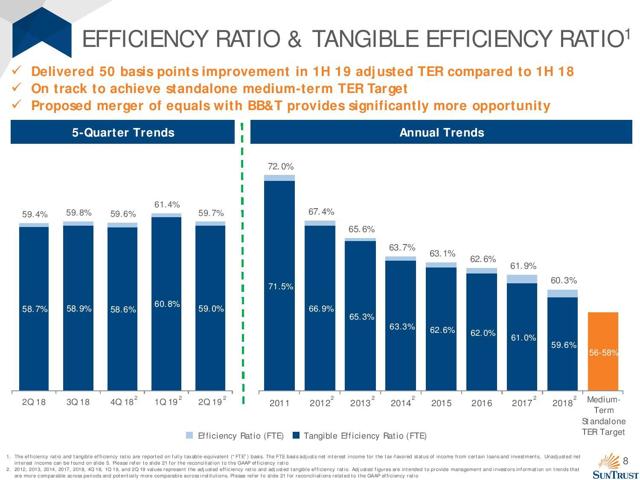

SunTrust has shown continued improvements in profitability with a 63.4% efficiency ratio for the second quarter. STI has seen a sequential decrease in its efficiency ratio over the last eight years, from a high of 72% to 60.3% at the year-end 2018. One area that SunTrust has invested heavily is in technology; these investments include automation, self-service services, and cloud-based systems.

The balance sheet remains strong, with the current ROE of 11.5% and ROTCE of 15.79%. Asset quality and capital remain strong with a NCO ratio of 0.22% and NPL (non-performing loans) of 0.34%. NCO and NPL continue to remain below historical averages, which reflects the favorable operating environment and underwriting discipline.

There has been a continued decrease in ALLL driven by slower loan growth and lower net charge-offs. All great signs of a bank showing restraint in its loan portfolio.

I like the fact that SunTrust can maintain a very strong capital position with its Common Equity Tier 1 ratio of 9.2% in Q2 2019, which is well above the regulatory requirement of 4.5%

Until the merger with BB&T, share repurchases are suspended and presumably will resume once the merger is complete.