Summary

- Coca-Cola's 2Q19 results were robust once again, with strength observed across the geographic segments, and on both volume and pricing.

- The company's product portfolio diversification seems to be playing a role in keeping the top line growing consistently, even in mature markets.

- I find KO a compelling buy due to its defensive nature, the company's solid performance, and a rich dividend yield.

- Looking for more? I update all of my investing ideas and strategies to members of Storm-Resistant Growth . Start your free trial today »

It has been yet another impressive quarter for Coca-Cola (KO), and the "sweet stock" is on the rise.

Ahead of the opening bell, on July 23, the Atlanta-based company delivered an all-around beat. Revenues of $10.0 billion topped consensus estimates by the widest margin of the past four quarters. Meanwhile, adjusted EPS of $0.63 came in two cents ahead of estimates. The outlook for the full-year was revised modestly to include a small increase in projected cash generation, but key items like comparable currency neutral net revenues and EPS remained largely unchanged.

Credit: Coca-Cola India

Credit: Coca-Cola India

Coke's not-so-secret recipe

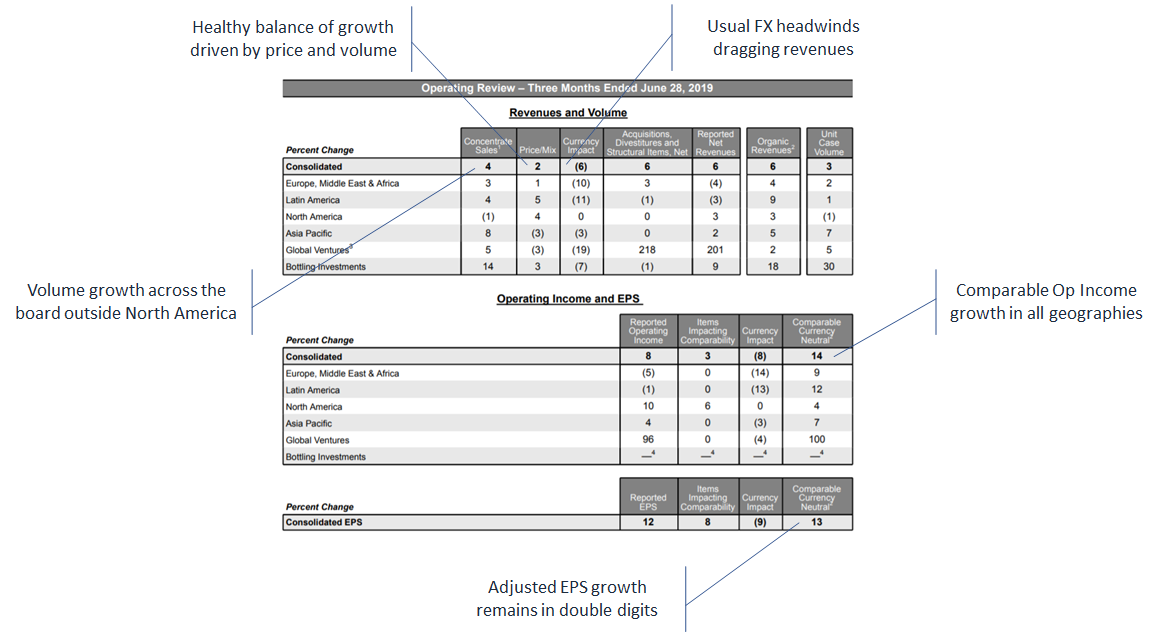

What perhaps impressed me the most about Coca-Cola's results was the consistency of the company's performance. Despite the usual FX headwinds, all geographies (i.e. North America, EMEA, Asia Pacific, and Latin America) experienced organic revenue growth of at least 3% in 2Q19, a commendable effort by a market leader in a mature industry. The drivers of top-line growth were also balanced, both on the volume and price sides of the equation.

Relative to my expectations, Coca-Cola seems to be doing a particularly good job in the most challenging and largest of segments: its home continent. Because North America is such a mature market for sugary beverages, the company's offerings outside regular soda seem to have been playing an important role in keeping revenues rising at a modest but consistent pace - including faster growing ready-to-drink coffees and Zero Sugar. It also looks like the company has been hanging on to pricing power in sparkling soft drinks, resulting in unit case volume pressure but improved margins.

Source: earnings press release, annotated by DM Martins Research

As the table above depicts, the consequence of mid-single digit volume growth, pricing and mix strength, and despite currency challenges, was reported operating income growth of 8% that I find encouraging. The figure would have been five percentage points better if adjusted for items like impairments and currency impact.