Summary

- PepsiCo continues to perform well despite most consumer packaged goods companies experiencing weakness.

- The company has returned almost 30% this year which is a rather large leap for a company like PepsiCo.

- I sold my position a few points ago and would love to own the shares again at the right price.

- The recent dividend increase and current valuation are not worthy of new investment dollars.

PepsiCo (PEP) shares have had quite the run this year. Along with many consumer packaged goods companies, the stock has elevated to levels that just don't make sense. Typically, investors are willing to pay higher than average valuations for these stocks in times of economic uncertainty or weakness. However, currently, the economy is chugging along as the CEO even stated himself. The stock offers a less than enticing yield as well as its shares trade at a valuation that would seem to leave little upside. Having sold my shares a bit early because of this belief, I do wish I held on. I do believe the opportunity will once again arise for me to purchase shares of PepsiCo; however, I decided to redeploy the capital from my sale into more undervalued stocks. Investors who liked the recent earnings report should hold off on initiating a new position. Investors who own shares may want to continue to do so, but, I believe a pullback will be inevitable.

Performance

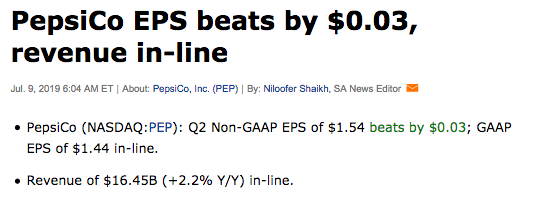

PepsiCo recently reported earnings that were reflective of strong operational management.

Source: Seeking Alpha

The company beat on both the top and bottom line and continued to show organic revenue growth. This comes at a time when many consumer goods companies are facing pressure.

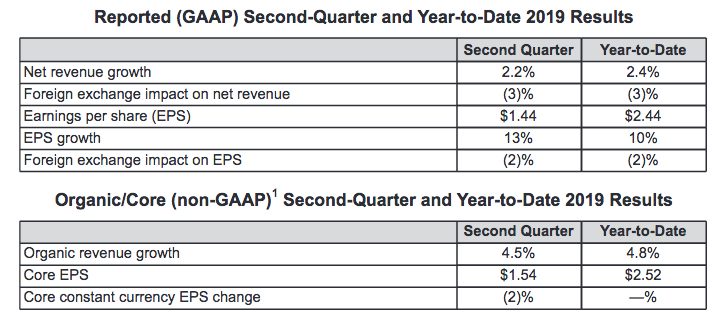

Source: Earnings Release

While this is certainly nice to see for investors, the strong growth is still not enough to stop earnings from actually declining this year. Due to various asset sales and franchising gains, and a higher tax rate, the company still sees earnings per share declining 1% this year. This while temporary should give investors pause as the company could perhaps have a hard time next year producing another great year of organic growth. Should the company see a slowdown in 2020 organic sales growth, earnings may not climb much again. The company expects 2019 earnings to come in around $5.50 per share. This is 3% lower than 2018 and includes a 2% impact for currency translations.

This also accounts for a strong share repurchases of $5 billion, which further helps boost earnings per share.