Summary

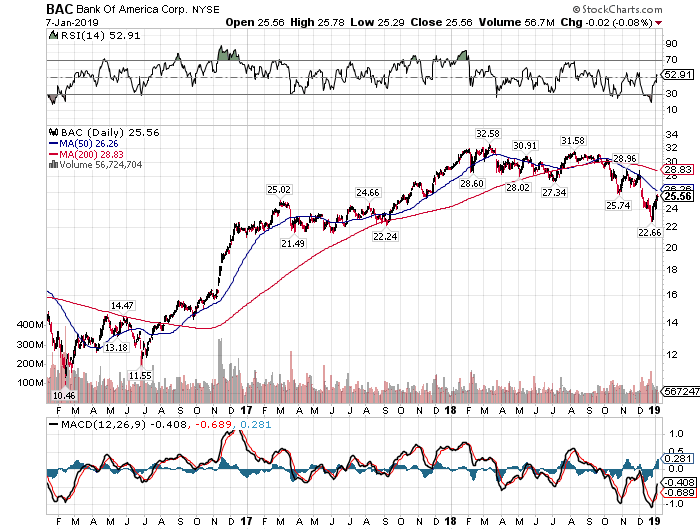

BoA is down over 20% from the yearly highs above $33.

Analyst projections haven't been cut, and the bank remains on track for $26 billion capital returns that provide downside protection.

The bank can double Q3 loss provisions and still grow EPS numbers.

The stock is too cheap at 9x '19 EPS estimates.

The large financials have taken large hits as the market is fearing a recession that causes an increase in loan provisions. Bank of America (BAC) is down over 20% from the highs above $33 earlier this year.

My investment thesis remains very bullish as the market has over-extrapolated too far on the risks, considering the profit cushion and stock buybacks at the large financial.

My investment thesis remains very bullish as the market has over-extrapolated too far on the risks, considering the profit cushion and stock buybacks at the large financial.